Spring Loaded

Navigating the tariff fallout

We're a week into the tariff bonanza and the markets are falling over. My view is that markets are overshooting to the downside at this point.

Walk with me...

Why tariff aren't about tariffs, and other misconceptions

All politicians have to play the hand they're dealt. And while ideology and personality of the players play a role in the outcome, the hand is in many ways a constraint.

And those constraints are dictated by factors outside the control of voters or officials. George Friedman and his team at Geopolitical futures, to name one, do a far better job of providing ample historical examples on this than I have the space for here. So whatever you think of President Trump, the GOP, the representatives in the house and senate, and all the other actors currently in the game... They are ultimately playing the hand they're dealt in my view. And as in most complex situations there are no guaranteed outcomes, but what we have today is a setup they must navigate. Stop fixating on the individual, start looking at the hand they’re playing.

With that, to the tariff policy. By now I'm assuming everyone has seen the math behind the proposed tariffs, which is based on the trade balance with a country. And sure, some chatGPT or similar may have been involved, and I'm enjoying the penguin memes as much as anyone.

Mostly though, the tariffs themselves don't really matter. They're the opening move in a process of a reshaping global relations. I'm with Ray Dalio on that one. That doesn’t mean I’m denying they are causing pain for consumers (not just American consumers for that matter), I’m saying I don’t believe this is the end state. And some countries, frankly, don’t matter in the grand scheme of things. Out of all the countries, the one that really matters is China. More on that later on.

The Framework backdrop

My framework runs at its core on a very simple equation. GDP is a function of People, Productivity and Debt. Those are the 3 big levers. I wrote the world's shortest summary on this before in the intro to this post on datacenters.

That equation is why the US, and most of the West, have a structural problem. You can measure it any number of ways: dependency ratio, labor market participation, spending patterns in healthcare, ... . They all boil down to the same underlying dynamic: we're getting older and we’re retiring.

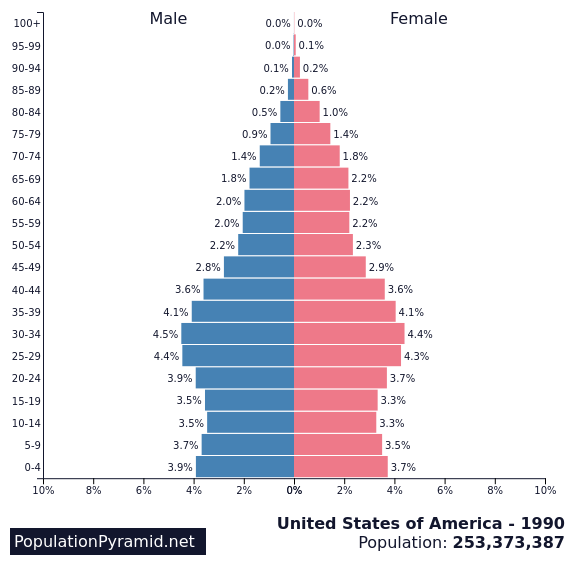

To really get this you need to understand the US population dynamics. Below is what that looked like in 1990, look at all those boomers in their 30s and 40s beavering away. And on the higher end of the pyramid, you can blame world wars for a significant imbalance between male and female. So a healthy workforce, without too much on the top to support.

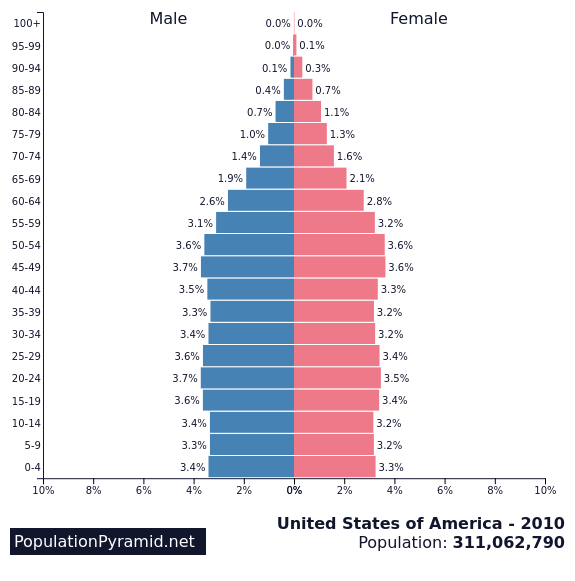

And now look at those same boomers retiring in 2010, leaving the kids born in 1980s and 1990s to pick up the retirement tab.

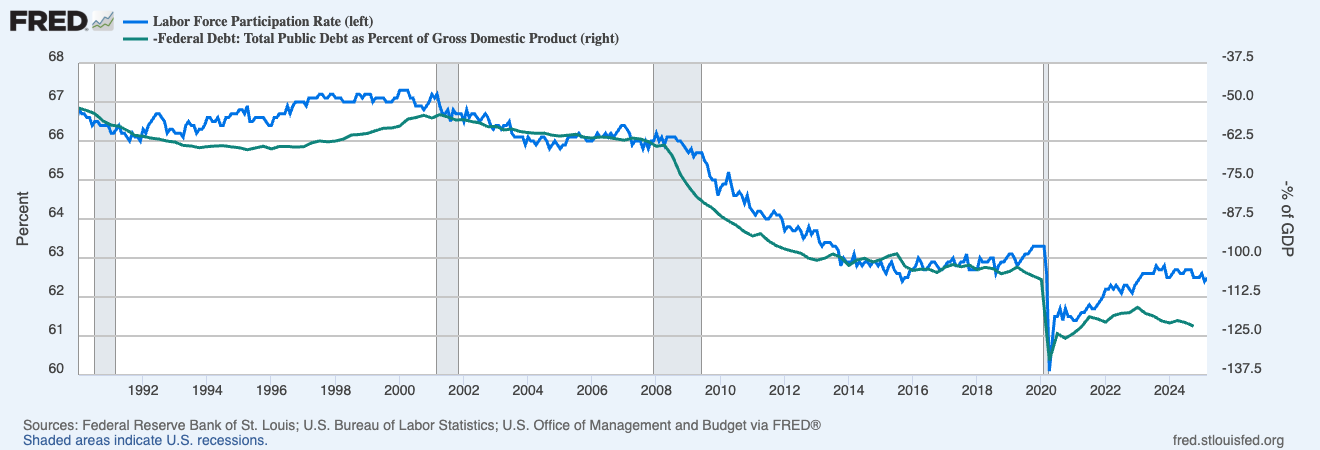

And right on cue, labor force participation dropped off from the mid 2000s for the next 15 odd years. The 2008 GFC didn't help, but this dynamic was always coming.

Here's a chart showing labor force participation (blue) with Public debt to GDP (green / inverted). Which has been closely correlated since the 1990s.

Remember it's either people, productivity or debt. And the first 2 are largely outside of the political class' control. So we’re compensating the lack of people with debt, regardless of which party was in charge. Talk about playing the hand you’re dealt!

This is the point where most people will start arguing about fading dollar dominance, unsustainable debt to GDP ratios, money printer go brrrr, ... and any other number of tropes. The hard reality is pretty simple. The US is living on a credit card to compensate the drop in productive people.

To sustain growth (and let's agree that that is a good goal) the US either needs more people in the labor force (or conversely, more boomers to exit stage left in a hurry while keeping population growth trends), more useful output per person (that's technology's job) or keep borrowing.

The issue of course with the latter option is that borrowing comes with those pesky future repayments.

How do you deal with repayments?

Well...if you're the government you have a couple ways of repaying debt.

There is the conventional way of decreasing people’s take home earnings to increase that of the government (tariffs, contributions, capital gains tax, wealth tax, national insurance, FICA, ... and any other name for what is all fundamentally tax). And then use these new earnings to repay the debt, and maybe even save a little by running a budget surplus. FYI…the last time the US managed to run a budget surplus was 2001. Strong economy (right before the .com crash) and still on the high end of labor force participation (so high income, and limited dependency to support) and a relatively restrained budget in terms of spending.

There is of course another way: devalue the currency. Sure there's discount math you could apply and fiddle with discount rates and time periods, if you're mathematically inclined. But as I put it in simple terms before: You give me a pair of Air Jordan's today and I repay you with a pair of off brand crocs in 10 years.

And like the proverbial frogs in boiling water, you want to gradually erode this. Avoid going full Weimar Republic and risk a popular revolt and the pain that comes from debasing currency too fast.

For most countries, playing with their currency mainly impacts themselves. The USD however is the backbone of global trade, so debasing this causes far more ripples. Any change in the dollar's value has a knock on impact on anything from commodities (they are priced in dollars, so a weaker dollar makes them cheaper in other currencies), import/export opportunities from/to the US (trade balance anyone?), dollar denominated debt (hello emerging markets). Generally speaking though, a lower dollar is broadly positive for global trade as it makes a lot of input materials cheaper in local currency.

Bringing this back to dealing with the US government debt. The ideal one-two punch is: borrow at the lowest possible rate to keep the coupon payments down, and then devalue the currency over the longer run to make the principal repayment essentially trivial. There are obvious constraints on this around the impact on both global trade and Americans, but intuitively you’d want to borrow at the lowest possible rate over the longest possible timeframe.

Which brings us to today. The US is looking at a wall of refinancing, about $9tn out of $36tn outstanding debt.

Part of this is the fallout of Covid. Go back to that chart above and look at 2020-2021, that sudden spike in debt is what we’re working with now. For reference, 5y notes issued in 2020 would have been sub 0.5%. 5y yield today sits at about 4%.

Obviously the US government doesn’t have $9tn in cash hanging about to pay off the debt. So we’ll have to put it on the new credit card. That's a meaningful change in coupon payments coming up, which will hurt the national budget for the next decade.

Lower yields would make a really big difference here! And incidentally, lower yields on US debt would also drive the dollar down, as US debt becomes marginally less attractive for investors. Bonus, as that has a net positive effect on trade, which ultimately is good for tax revenue from US businesses and consumers.

In short, the playbook here is: dollar down, yields down, slow erosion of the debt.

I’ve argued before that the ultimate release valve is a productivity boost of biblical proportions. As a former CTO, I am predisposed to believe that technology is what will get us there. I doubt it will be the AI claims people are making today, but on balance I'm a techno-optimist and a structural bull on that sector for this reason. And I’ll deal with the wild hype from time to time.

China needs a weaker Dollar

Anyway, this was a long prelude to talk about tariffs and China. Which is the one country on that list that matters far more than all others; if not exclusively.

First and foremost, China owes about $1.1tn in dollar denominated debt. In other words, it needs USD to pay that back. And of course, a lower dollar makes that a little easier. It does hold close to $800bn or so in US Treasuries as well. That’s a source of USD, and if they dumped it on the market US yields would spike. But it would also rob them of a steady source of USD. So as all things, balance. Any violent unloading of debt will hurt the US but won’t be pain-free for China either.

The second aspect is its own economy.

A large part of the Chinese economy is still built on being the workshop of the world, and is loaded with debt. That doesn't mean China overall is weak, but the technologically advanced segment is too small to make a true national difference on this data.

So yes, there is still growing GDP but no longer at the rates it needs to handle the amount of debt in their economy. I won't repeat it all here, but Rand wrote a great piece on the split in China's economy between old and new.

All this to say, the Chinese need to stimulate their own economy by injecting liquidity. And that's where the squeeze is. China manages the RMB in a range against other currencies, including the dollar. So injecting RMB in the system (and thereby lowering the currency’s value) would mean being forced to either let the currency devalue in public or compensate by having more foreign reserves. The latter is a costly operation on a strong dollar. However, if the dollar was to ease it creates a gap for the Chinese to devalue their own currency and create some much needed economic impulse.

Btw, Chinese 10y yields are near the 1.5% mark at this stage down from nearly 5% in 2015. So everyone is structurally buying 10yr bonds. Or bluntly, people are expecting lower growth. The likely reaction, balance sheet expansion. Or simply put devaluing the currency, which also allows them to get out of some debt much like the US.

Oh, and tariffs? The other way the Chinese earn USD is through export. The US effectively exports USD to China in return for low priced goods. Guess what tariffs would choke off.

You think the US has no leverage over China? Guess again.

I'm sure the politicians on both sides will do the necessary chest thumping in the press, everyone's a strong leader after all, but eventually reality will sink in and we will get a deal.

As any high stakes negotiation, it will get nasty, there will be mud slinging, insulting, walking away from the table only to return later, ... . But ultimately, they need a deal as much as the US needs them to accept one.

The coil is winding

Since ultimately I'm in the business of making money first and opining second, let's start talking about the structural trade setups here.

At heart, business performance broadly lags economic conditions. So with that, the entire business cycle is a function of

Credit. Both base rates of the government which act as a base for commercial loans, as well as credit spreads which speak to expected returns for risk.

Specificlaly the 10y matters here as that's the base for risk-free in most models, and the mortgage market

Dollar strength vs other currencies. It affects commodity prices and a large slice of global trade.

FED actions. Is policy net adding or removing liquidity. Doesn't matter if that's QE/QT, or through Repo action or straight up balance sheet expansion. It's all either moving money in or out of the economy. The mechanics are complex, the end results far less so.

Commodities but in particular oil, copper (uptick in industrial activity should see an uptick here) and gold (inverse, rising gold price is a flight to safety)

There are more I could add to the list (Baltic Dry, Emerging market credit spreads, VIX and other main market indexes outside the US to name a few) but to a large extent the above list will capture the core action.

So let's see what happened there recently

Oil is at $60 / barrel, down from $70 earlier this year.

Gold has ripped up 50% since early 2024 but is starting to look a little stretched finally. It actually sold off 3% on tariff day and day+1.

Copper is down 17% since 1st April

Yields across the curve dropped on tariff news but are now more or less back. 10y yield is still down 50bps for the year.

DXY lost about 2% on tariff day and is down 5% over the last 3 months after a big run up in Q4.

FED actions tbd, but I doubt they're leaning towards raising rates aggressively at this stage.

In other words:

We have coiled the spring with some of the loosest conditions possible at this stage. And we have done so in a rather violent squeeze.

The only question left in my mind is when it unleashes. Because when it comes, it will come fast.

Let it rip

We've seen the cliff edge, we jumped off, we fell into the air pocket. Now it's time to hit the rebound.

I've long said I'm structurally bullish on the US for the rest of the year, and we're not looking at a recession. I'll hold that view until the data changes.

We’re at the point where it's almost impossible in my mind to not just be irresponsibly long and do well out of it on a 6 month horizon.

I think in the next few days and weeks, we'll get a rebound that is more sentiment driven than anything. Sentiment indicators and market breadth are all at levels that we haven't seen since 2008's GFC. That's too far for the risk we see today based on the overall data. AAII retail sentiment is max bearish, UMich consumer sentiment is in the 50s, that’s depression levels. Nearly all stocks in the SP are below 20 & 50 day moving averages, New High / New Low dropped to levels only surpassed at the depths of the covid and GFC capitulation.

The durable upswing might trigger on some positive news with regards to the China conversation. The broader investor community might just figure out that underneath the noise sits a lovely set of data. Maybe we need the next few readings of business surveys. The short term swing will be news driven. A glimmer of hope is all we need at this stage.

And looking ahead, the upcoming earnings in April are going to be great for every executive to downplay expectations for the rest of the year. While that is certainly warranted, it also will lower the bar for beats later in the year.

For my money, I'll stay overweight on IWM and I'll get another nibble at broad tech indexes. That's in line with the historical outperformance for this stage of the early cycle with very easy financial conditions.

In the same framework, emerging markets and commodities should outperform on dollar weakness and an uptick in global activity.

While you can't go wrong with SPY, I think performance there will lag on account of some stragglers and the top heavy big-tech nature of the index right now.

So...it's all good?

Nothing is ever certain of course.

At a minimum, the ongoing conversation with China is one to watch. Both how it is played out in the media, which will affect sentiment, and how any trade agreements shape and shift. We may end up in an escalating tariff war that drags on and will start to bring substantial pain. As I said before, my view is that both sides need a deal and so I think it's unlikely they'll want to drag this out for too long. Duration, rather than the absolute level of tariffs is the main risk here.

And talking of escalation. A remote but non-zero risk would be if tariffs spill over into actual war. The kind with tanks and soldiers. A remote possibility in my mind, but all bets are off if we go there. On the other hand, I'm not sure the market will matter all that much if we do end up in a conflict where both the US and China are waging all out war.

I know tariffs are inflationary. I wrote about this before, this type of inflation is different. Tariffs don't comply with the demand-driven style inflation that is typical in a normal business cycle. In fact, tariffs create a potential drag on demand that could lead to less trade overall (coincidentally, that's also a dollar weakener). It means the FED's usual response of raising rates has no real effect on this type of inflation. The FED knows this too, don’t hold your breadth for the FED to raise rates.

We'll have to keep an eye on earnings in Q1 including guidance. As I said, I expect Q2 and Q3 to produce beats, but that remains to be seen. I do think good news heading into those will be discounted quickly by the market. So market dynamics during Q2 might hold a clue there already to see if the thesis holds.

I opened The Perfect Storm with "tariffs come, tariffs go". Maybe I should have added option 3: tariffs keep coming. The ease with which this administration announces (or tweets, in effect) new policy baffles me. And so on any given day, the penguins could probably get tariffed some more. And higher tariffs will eventually hurt American consumers. I think the bigger question here is still around certainty rather than the exact tariff level. If the administration sticks to deals made with countries, it will become clearer that they are open to negotiate and settle. Backtracking on mutual agreements would be the surest way to increase and sustain uncertainty. And if there's one thing business doesn't like ...

Closing note

I wrote this article initially on the 8th of April and shared it in a private group, followed by opening some starter positions in QQQ, XLE and IWM. We’ve seen the first bit of that coil unwinding by now, though I don’t think we’re entirely through that yet.

I am holding my broader thesis that the US will look strong for most of the year. Even more so now that tariffs have created extremely loose conditions.