The perfect storm

...in a teacup

I’ve been called many things over the last 2 decades, but rarely was optimist part of the list. Yet, here I find myself feeling positive about US equities performance in the remaining 9 months of the year.

Here’s a bit of a random walk down my thinking

Tariff day

It’ll come (I’m writing this before the announcements). It’ll go. On balance, it will more likely reduce the chaos than add to it.

The whole thing is classical TV drama. It’s the apprentice Tarif Edition. All eyes on the chaos, maximum speculation, zero certainty, big reveal. Maybe I’m jaded, but those events in life rarely live up to their buildup.

And in terms of the build up. AAII sentiment sits north of 60% bearish, UMich sentiment sits at 57, and inflation expectations have skyrocketed (mind you, truflation keeps trundling along at the bottom…). Those levels are deeply bear market levels, and we’re only 10% or so off the high in the S&P. A correction for sure, but far from an all out soup-lines-for-everyone level depression.

The last ISM report was full of interesting goodies. But one thing stood out in the comments section: Everyone is holding tight on account of uncertainty around tariffs. Not on tariffs per se, but on what might be.

Rotation

Right now the market is historically speaking very top heavy. The top 5 stocks represent about 25% of the index currently, historically the average is closer to 14%.

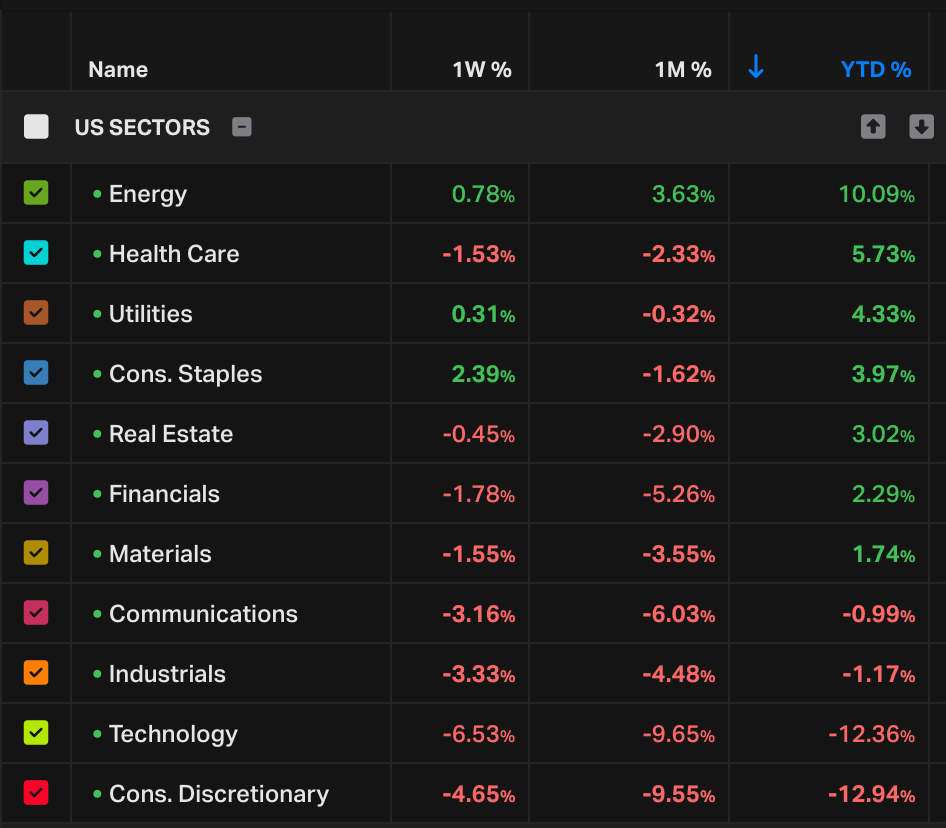

And as you can see from the breakdown below, YTD the money’s been flowing out of predominantly the big tech boys hiding in Technology and Discretionary; and piling into Energy. And that’s with an oil price around $65-$70 per barrel.

or even more telling… That’s a lot of YTD green there. Far from a broad capitulation.

Tariff, part 2

The other interesting read between the lines is driven by the new orders. New orders dramatically expanded in December and Jan and then pulled back in Feb and March.

If you’re running a business and you know tariffs may or may not in some way show up in Feb end March, the rational thing to do is to stockpile some of your inputs.

So we’ve seen some of the natural demand of Feb & march shift into December and January.

Here’s a hypothetical CEO:

I’m sitting on input materials at pre-tariff costs

tariffs come into play, so I can charge more for my products and blame passing on some of the tariff costs (note: historically the tariff is never passed 100% to the consumer, so let’s say we’re bumping 10%)

My margin for the next quarter just went up, short term boost to earnings

Debt refinancing

It’s no secret the US government has a large amount of debt to refinance. About $9tn, on an overall $36tn debt. And as president Trump likes to remind people, he’s the king of debt and prefers low rates.

So how do you get low rates if your the president?

Well, you take the growth out of the economy in the short term. And then assume the FED cuts rates because it _looks_ like they have to.

Longer term

A couple of datapoints to note, despite the gloomy ISM reading this month

Overtime hours keep creeping up from the lows in 2024

LAX container traffic grinding higher YoY, we’ll see how tariffs start to impact this

Swedish PMI, a heavy export economy, is holding at mildly expansionary levels

Financial conditions are still easy. They worsened slightly in February, but we’re far off from the steep climb into the levels that would signal deep troubles

US money supply had a bad month in December, but in Jan and Feb is back at levels of expansion it was in 2018 now.

So in short, there is still plenty underlying data to be positive about the future.

Drill baby

I noted earlier that rotation is happening into energy, even with oil at current levels. One of the energy surveys remarked that drilling in the US at this oil price isn’t something the industry would jump on; despite Trump’s “drill baby drill” rallying cry.

So all else equal, we have money moving into oil and industrial activity picking up in the US which should demand more oil. And suppliers who aren’t yet willing to drill more at these levels. Economics 101 … rising demand on a static supply equals rising prices.

It’s not all bad. Hold the longs, look to add as we ideally bottom out on bad news in the next few weeks.